Egypt’s real estate market is witnessing robust demand, as a result introducing new city developments as part of large-scale real estate projects, according to Fitch Solutions’ Egypt Real Estate Report.

The report, which includes five-year forecasts extending to 2024, noted these new large-scale projects include the New Administrative Capital (NAC), New Alamein, and New Mansoura.

Fitch added that the ongoing development and construction of 20 new cities across Egypt, in addition to the development of the 23 existing new cities, present attractive investment opportunities in the country.

The impact of the novel coronavirus (COVID-19) pandemic is expected to be far less than Egypt’s western counterparts. This has been attributed to Egypt’s never having gone into full lock down during the first wave of the virus in the first half (H1) of 2020.

Despite lower GDP and household spending levels remaining flat, Fitch added that it expects growth in rentals to remain positive in 2020. Demand for retail units will subsequently improve, with rental rates increasing in general.

“Egypt is the second biggest recipient of foreign direct investment (FDI) in Africa and the Arab world, according to the UN’s World Invest Report, and the Egyptian economy’s headline growth is stable despite the pandemic,” the report read. “Real GDP will continue to outperform the region, averaging 2.6% in fiscal year (FY) 2019/20 (ending 30 June) and 3.6% in FY 2020/21. This would place Egypt as one of the strongest growing emerging market economies in the long run, which we believe will boost the demand for commercial real estate.”

Fitch forecasts that office rental growth rate to remain in the positive, albeit at a lower rate. It further projected that greater macroeconomic stability will lead to an increase in international investment into Egypt’s non-residential sector.

This would, in turn, breathe life into the Egyptian government’s various economic diversification projects spanning industrial, tourism and commercial infrastructure.

“Residential development will largely remain the domain of the state, owing to the fact that large-scale housing projects must be affordable enough for the average Egyptian,” Fitch said. “Moreover, Egyptian commercial real estate assets have been somewhat resilient to the COVID-19 pandemic, due to previous higher government investment spending, rising natural gas production and an improving regulatory environment.”

The report added that, a dearth of investment grade assets restricts available options for occupiers and investors. Limited new supply in 2020 will help narrow the supply gap and support demand for commercial real estate stock.

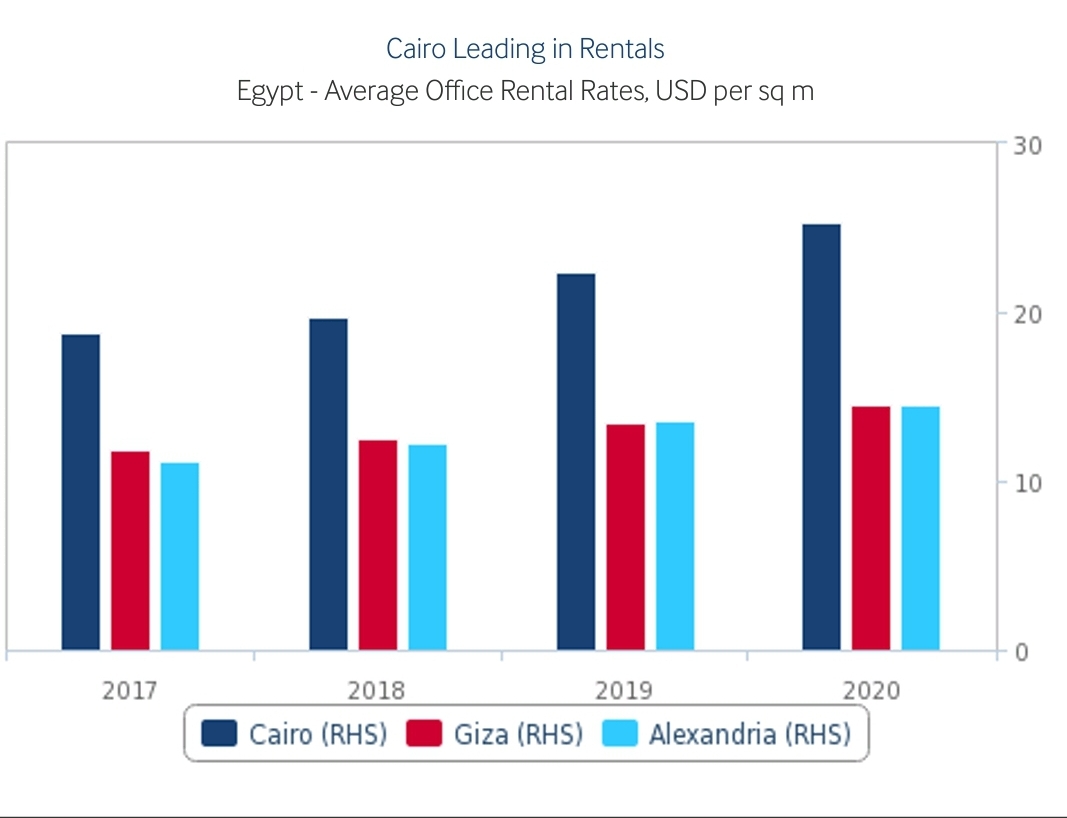

The report expects that supply will be absorbed by the market fairly quickly. Rental rates are set to increase across all three cities in all three sub-sectors despite bleak global economic conditions.

Cairo remains the epicentre of commercial real estate market activity, with investors actively looking for opportunities in the New Cairo sub-market, where there is a steady delivery of investment grade office assets. Stable rental rates and favourable yields still provide good opportunity for new and emerging players in the market, according to the report.

Fitch sees the investment potential in Egypt’s office sub-sector, with the continued expansion of the non-oil sector. There have also been favourable reforms, providing the necessary stimulus to drive business activity, leading to stronger demand for office spaces.