The IMF released on Tuesday its latest Regional Economic Outlook (REO) where it mentioned that debt will remain very high in a number of countries, particularly Bahrain, Egypt, Jordan, Lebanon, Mauritania, Morocco, Pakistan, Sudan, and Tunisia.

The report added that the importance of addressing the debt burden is also illustrated by the significant gains from fiscal adjustment being lost through rising interest payments, adding, “accordingly, going forward, a significant fiscal adjustment is still needed.”

Bilateral and multilateral official financing has supported reserve buffers in several countries in Egypt and some other countries, added the report, noting that tourist arrivals have risen steadily following improvements in security, a weaker exchange rate, and a resumption of direct flights from Russia.

Moreover, the report mentioned that the MENAP oil-importing countries issued about $12bn in sovereign bonds in the first half (H1) of 2018, covering approximately two-thirds of the planned borrowing for the year, and almost $3bn more than in 2017.

“This reflected borrowing by Egypt and Lebanon of $6.5bn and $5.5bn, respectively, amid favourable external financing conditions earlier this year,” noted the report.

The market anticipates issuances from other countries in the region later this year. However, this could prove challenging as emerging market (EM) financial conditions have tightened, added the report.

Pushing energy subsidy reforms to completion will be critical, including by enacting automatic fuel pricing adjustment in Egypt and Tunisia, to avoid the risk of reversal and create space for more growth-friendly capital spending.

“This should be coupled with increased spending efficiency through strong evaluation, prioritisation, and implementation of infrastructure projects. With global financing conditions becoming more uncertain, deepening domestic bond markets could help reduce future financing risks,” mentioned the report.

Looking ahead, apart from Egypt and Tunisia, domestic demand will increasingly become the main driver of growth, as contributions from the external sector fade, mentioned the report, adding that several factors will sustain private consumption, including growth in remittances in Egypt, Lebanon and Tunisia.

Looking ahead, apart from Egypt and Tunisia, domestic demand will increasingly become the main driver of growth, as contributions from the external sector fade, mentioned the report, adding that several factors will sustain private consumption, including growth in remittances in Egypt, Lebanon and Tunisia.

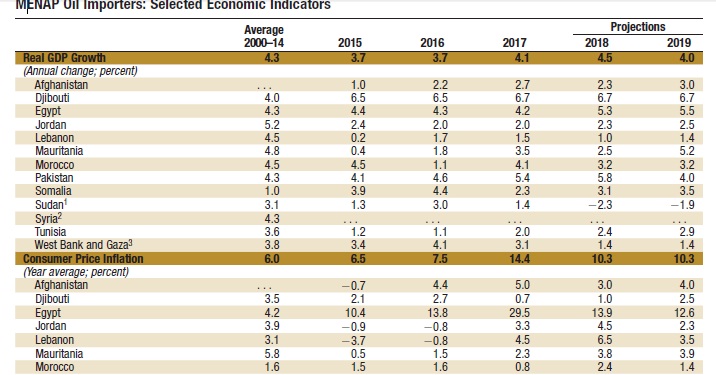

Monetary authorities in the region have largely maintained a neutral or tightening monetary policy stance in Egypt, Jordan and Tunisia that remains broadly appropriate, said the report noting that the countries will need to remain vigilant against a rise in inflation, and stand ready to anchor inflation expectations should second-round effects from higher energy and food prices materialise.

The region’s low productivity informal sector

A large section of the economy in the region is dominated by a low productivity informal sector, with the formal sector accounting for only a third of employment in the region, said the report, noting that businesses with five or fewer employees dominate the private sector in Egypt which represents about 60% of the companies.

However, the informal sector has difficulty accessing credit, market opportunities, and government services, and this limits the vibrancy of the private sector, said the report, adding that tight labour market regulations impede firms from expanding and gaining economies of scale, constraining most small businesses to informality.

Moreover, the government loses out on revenues since this sector remains largely untaxed, asserted the report.

For the main improvements in the macroeconomic and structural reforms, the report mentioned improving competitiveness through exchange rate adjustments in Tunisia, easing access to credit in Egypt, Morocco and Pakistan and industrial land in Egypt, and diversifying the economy in Mauritania.

The report said the above mentioned measures among other measures, would help the private sector compete more effectively, better enabling it to take advantage of external demand.

Social spending is relatively low across the MENAP region

Some countries as Egypt, Jordan, Pakistan, Oman and Saudi Arabia have coupled subsidy reforms with strengthening targeted social safety nets to enhance the equity of reform and support growth, mentioned the report.

It is notable that the level of social spending is relatively low across the MENAP region. In contrast, social spending in the CCA is comparable, mentioned the report.

The adoption of new procurement laws in Egypt and Saudi Arabia will increase the transparency of public procurement and enhance public oversight, said the report, noting that this will help increase the efficiency of public expenditure and improve fairness in the selection process, both of which will support growth.

Better perceptions of government accountability can also help reduce the cost of borrowing for both the sovereign and the private sector, further boosting investment and growth

Growth projections for the oil importers, exporters

Growth projections for the oil importers, exporters

Oil exporters in the MENAP will experience visible improvements in external and fiscal balances in the years of 2018, 2019 amid higher oil prices, said the report, adding that despite a significantly weaker outlook for Iran given the re-imposition of sanctions, oil-exporting countries are projected to grow at 1.4% in 2018 and 2% in 2019.

Among Gulf Cooperation Council countries (GCC), following a 2017 contraction, growth is expected to recover to 2.4% in 2018 and 3% in 2019, noted the report, adding,” This is underpinned by a recovery in non-oil activity, supported by a slower pace of fiscal consolidation, and stronger oil production.”

Growth is expected to continue at a modest pace of 4.5% in 2018 for oil-importing countries in the MENAP region, before dropping back to 4% in 2019, mentioned the report.

Continued strong growth in Egypt and Pakistan in FY 2017/18 is driving the regional aggregate growth higher, masking weaker and more fragile growth in other countries, particularly those affected by conflict or its spill overs such as Afghanistan, Jordan, Lebanon and Somalia, said the report

The region’s exports and imports

Steady export growth has helped mitigate the impact of higher oil prices on the region’s external balance, said the report, noting that the current account deficit is expected to edge down to 6.5% of the GDP in 2018, from 6.6% last year, and decline further to 6.1% in 2019.

Annual export growth in 2018 is projected to more than double from last year to 15.4%, outpacing import growth of 10.1%, up from 8%, said the report, adding, “this surge is largely driven by Egypt, reflecting base effects from receding macroeconomic imbalances during 2016 and 2017 and an improved business environment.”

More broadly, growth in Europe has supported an increase in exports across the region, said the report.

Growth risks over the MENAP

Growth in MENAP region is uneven, with about three-quarters of oil-importing countries expected to grow at less than 5% over the medium-term, which is too low to address the region’s employment challenges and developmental needs, affirmed the report.

Higher oil prices are also offsetting some of the underlying improvements in external and fiscal balances, said the report adding that multiple and intertwined risks cloud the outlook of the MENAP region.

The report explained that the risks include a faster-than-anticipated tightening of global financial conditions, escalating trade tensions that could affect global growth and hurt key MENAP trading partners, geopolitical strains, and spill overs from regional conflicts.

The risks could trigger a deterioration in financial market sentiment, and greater financial market volatility, aggravating the financing challenges for countries with high levels of debt or large refinancing needs, noted the report.

Political uncertainty and social tensions could also challenge the reform agenda in some countries, said the report, adding, “there is considerable uncertainty surrounding the outlook for oil prices. If they continue to increase, that could weaken the resolve of oil exporters to continue reforms, while exacerbating pressures on oil importers.”

IMF’s recipe for tackling the region’s risks

The MENAP countries must commit to further reforms in order to strengthen their resilience against these risks and build a future where the benefits of growth are shared by all, said the report.

Flexible exchange rates should serve as buffers in the event of external pressures, said the report, adding that additional fiscal adjustment is needed throughout the region in order to build and strengthen buffers, safeguard sustainability, and achieve greater intergenerational equity.

“Countries could do more to ensure that fiscal policies are equitable and are more supportive of growth. The outlook and the rising risks underscore the need to intensify efforts to raise growth to levels that generate enough jobs for the benefit of all,” mentioned the report.The report said that countries should expand access to finance, strengthen governance, improve education outcomes, and enhance labour market flexibility, particularly in the GCC.

To ensure that future fiscal adjustment is as growth-friendly and equitable as possible, countries need to prioritise expenditure on growth-enhancing and high-quality investment in human capital and physical infrastructure, while sustaining well-targeted social spending, said the report.

The countries should move to a more progressive tax structure, diversify the revenue base, and eliminate distortions, added the report.