Egypt’s real estate market witnessed a significant surge in the first half (H1) of 2025, with the country’s top 10 developers achieving combined sales of around EGP 651bn, compared to EGP 442bn in the same period of 2024 — marking a growth of 47%, according to a new report by The Board Consulting, a market research firm.

The report highlighted that this leap underscores the ability of leading developers to strengthen their market share at the expense of small and medium-sized competitors. It also reflects a shift in customer behaviour, as buyers have become more selective and increasingly gravitate toward trusted brands with strong track records.

According to the report, the performance of these top players further consolidates their dominance in Egypt’s property sector, enabling them to remain resilient despite ongoing economic challenges.

It added that the average ticket price of residential units sold by these developers in H1 2025 stood at about EGP 17m, up 7% compared to the same period in 2024, illustrating a clear focus on targeting affluent segments of the market.

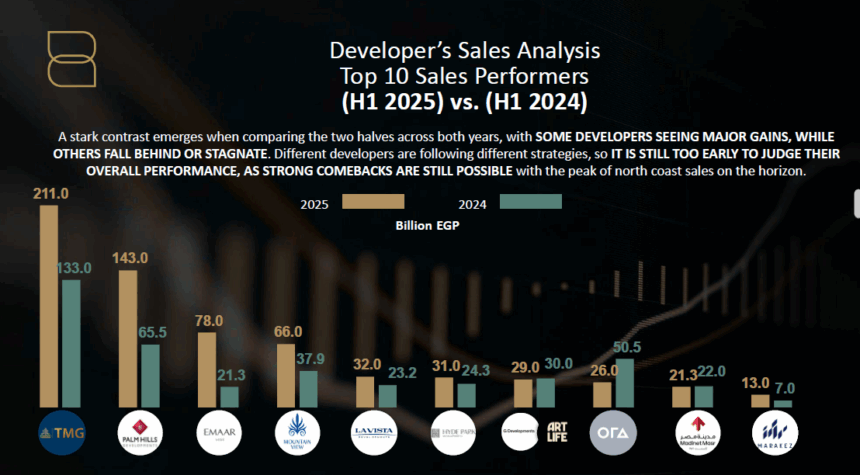

Talaat Moustafa Group (TMG) maintained its position at the top of the ranking, recording sales of EGP 211bn in H1 2025, compared to EGP 133bn a year earlier. This 59% surge reflects the group’s strong project pipeline and the successful timing of its launches.

Palm Hills Developments came in second, posting sales of EGP 143bn — more than double its performance of EGP 65.5bn in H1 2024. The company benefited directly from the broader market upswing, as well as strong demand for its flagship projects.

Emaar Misr secured third place with sales of EGP 78bn, up from EGP 66bn in the same period last year, reflecting consistent and steady growth.

Mountain View recorded one of the most notable jumps in performance, rising to EGP 65.7bn compared to just EGP 21.3bn in H1 2024, signalling exceptional demand for its projects and effective market positioning.

La Vista followed with EGP 32bn, up from EGP 23.2bn, while Hyde Park Developments climbed to EGP 30.7bn from EGP 24.3bn.

G Developments, however, recorded a slight decline, with sales of EGP 29bn versus EGP 31bn in H1 2024. Similarly, Ora Developers witnessed a sharp drop, posting EGP 26.2bn compared to EGP 50bn in the same period last year, indicating a slowdown in sales momentum.

Madinet Masr for Housing and Development achieved EGP 21.3bn in H1 2025, broadly in line with its performance of nearly EGP 22bn in H1 2024, reflecting modest but stable activity.

Rounding off the top 10, Marakez posted EGP 13.4bn in sales, nearly doubling its performance from EGP 7bn in the first half of 2024.

The report concluded that the strong performance of Egypt’s top real estate developers demonstrates their resilience and strategic positioning in a competitive market. While a few players experienced declines, the overall trend highlights market consolidation in favour of the largest and best-capitalised firms.

With rising demand for high-value residential units, ongoing urban expansion, and buyers’ increasing preference for established developers, the sector is expected to sustain growth momentum in the second half of 2025, despite persistent challenges such as inflation and rising construction costs.