Egypt’s real estate market entered a more measured phase of growth in the first quarter (Q1) of 2026, as the sector adjusted following several years of rapid expansion fuelled by aggressive project launches, flexible payment schemes, and strong investment inflows from Gulf markets.

According to a new quarterly report by The Board Consulting, the market is transitioning into what it describes as a “healthy correction phase”, with performance increasingly concentrated among large, financially robust developers, while smaller and mid-sized players face mounting challenges amid tighter liquidity conditions and more selective demand.

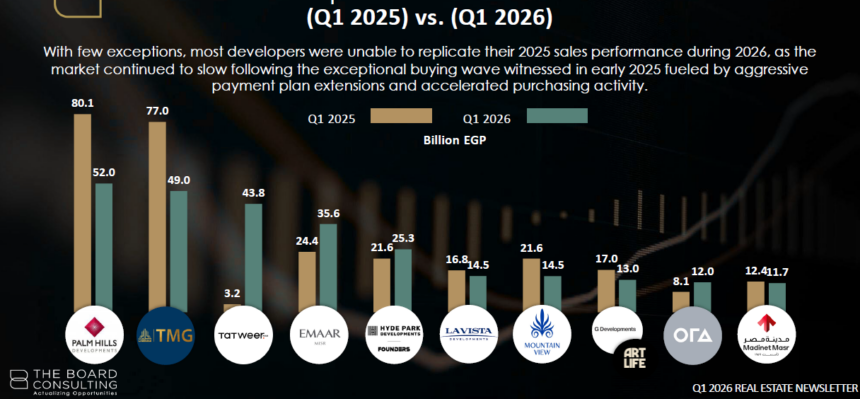

The report revealed that total contracted sales among Egypt’s top 10 developers reached approximately EGP 271bn during Q1 2026, compared to EGP 290bn in the corresponding period of 2025, representing a year-on-year decline of 6.5%.

Despite the slowdown, sales levels remain significantly higher than those recorded in Q1 2024, indicating that demand has not weakened fundamentally but has shifted towards more selective and value-driven purchasing decisions.

Unit sales mirrored this trend, declining by around 15% year-on-year to approximately 15,500 units. The decrease reflects growing buyer caution amid rising property prices, macroeconomic uncertainty, and evolving financing conditions.

Industry analysts noted that the market is no longer driven solely by volume growth, but increasingly by what they describe as “quality absorption”, with developers that possess strong balance sheets, credible delivery records, and established reputations continuing to capture the largest share of demand.

Macroeconomic and Regional Environment

The broader economic backdrop continues to shape Egypt’s real estate dynamics. Regional geopolitical tensions, fluctuating capital flows, and ongoing currency adjustments have created a more complex investment environment for both developers and buyers.

At the same time, Gulf sovereign and private capital continues to increase exposure to Egyptian assets, particularly through large-scale coastal developments and mixed-use urban projects. This trend reinforces Egypt’s position as a long-term investment destination despite near-term market volatility.

In response, developers are recalibrating pricing strategies, adjusting unit sizes, and adopting phased development models that better align with changing demand patterns and affordability considerations.

East Cairo Maintains Leadership

East Cairo retained its position as the country’s leading real estate sales hub, generating approximately EGP 130bn in contracted sales during the quarter. Demand continued to be supported by integrated residential communities and proximity to major infrastructure projects and emerging urban centres.

The North Coast ranked second with around EGP 50bn in sales, reflecting continued momentum in coastal developments and strong investor appetite for holiday homes and second-residence products.

Ain Sokhna recorded approximately EGP 40bn in contracted sales, supported by strong-performing projects and growing tourism-linked residential demand. West Cairo contributed roughly EGP 30bn, maintaining stable activity levels but remaining less dominant than the eastern expansion corridor.

Leading Developers Strengthen Market Position

The competitive landscape continues to consolidate in favour of Egypt’s largest developers, with a widening gap emerging between top-tier companies and mid-sized market participants.

Palm Hills Developments led the market with EGP 52bn in contracted sales, supported by strong performance across its East Cairo and New Administrative Capital projects, alongside an expanding coastal portfolio.

Talaat Moustafa Group (TMG) followed closely with EGP 49.1bn in sales, driven by sustained demand across its existing developments despite limited reliance on new project launches during the quarter. The company continues to benefit from strong brand recognition and a large recurring customer base.

Tatweer Misr secured third place with EGP 43.8bn in sales, supported by strong momentum in Ain Sokhna and continued marketing activity targeting premium residential segments.

Emaar Misr ranked fourth with EGP 35.6bn in contracted sales, maintaining its position in the high-end residential market. Hyde Park Developments followed with EGP 25.3bn, reflecting steady demand and consistent project execution.

Meanwhile, La Vista Developments and Mountain View delivered stable performances, while ORA Developers and Madinet Masr completed the top rankings with solid, albeit more moderate, sales results.

Shift Towards Premium and Coastal Projects

The report highlights a growing strategic shift among developers towards premium offerings and coastal expansion, particularly along the North Coast and the Ras El Hekma corridor, which is rapidly emerging as one of Egypt’s most competitive real estate destinations.

Large-scale partnerships, international collaborations, and hospitality-led mixed-use developments are expected to define the sector’s next growth phase. Developers are increasingly competing on factors beyond pricing and payment plans, including branding, lifestyle integration, and destination creation.

The market is also witnessing the emergence of new corporate structures and joint ventures, as established players expand into new geographical markets and customer segments.

Evolving Consumer Preferences

According to The Board Consulting, consumer behaviour is undergoing a significant transformation. Buyers are becoming more cautious, research-oriented, and focused on developer credibility, delivery performance, and long-term value preservation.

As a result, developers are moving away from purely sales-driven marketing approaches towards more sophisticated strategies built on data analytics, customer segmentation, and brand positioning.

To support this shift, the consultancy has introduced new analytical tools focused on brand perception and psychographic segmentation, helping developers gain deeper insight into evolving customer preferences and purchasing behaviour.

Despite the short-term moderation in sales activity, the report suggests that Egypt’s real estate market is entering a more mature stage of development rather than experiencing a downturn.

The coming period is expected to be characterised by greater market consolidation among leading developers, increased product differentiation, and intensifying competition within premium and coastal segments.

While economic volatility remains a key challenge, Egypt continues to strengthen its position as a regional real estate investment hub, supported by large-scale infrastructure development, foreign capital inflows, and sustained urban expansion.