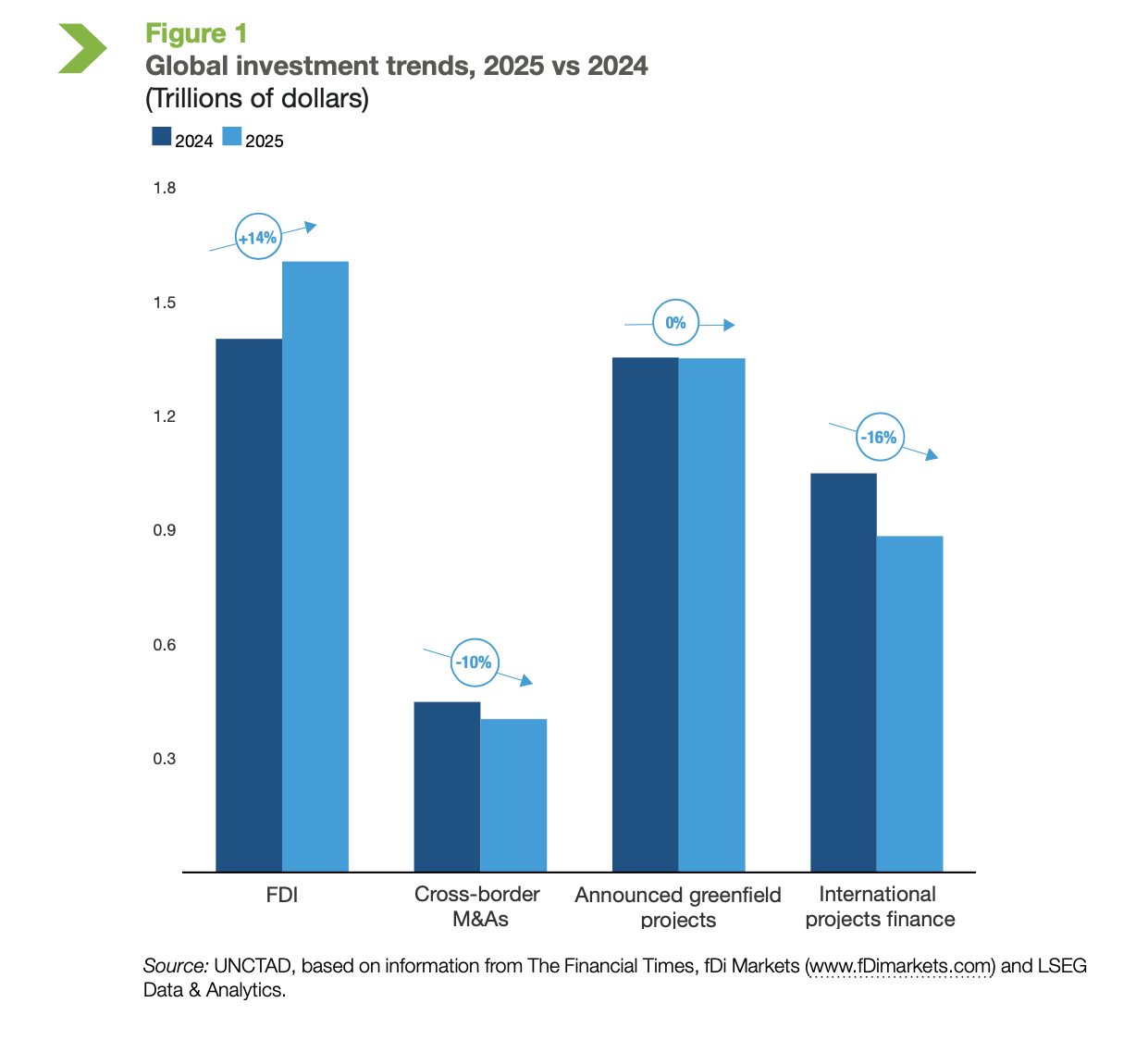

Global foreign direct investment (FDI) rose 14% to an estimated $1.6trn in 2025, though growth was concentrated in developed economies while Africa saw inflows plummet by approximately one-third.

Egypt maintained its position as the largest FDI host on the African continent, attracting $11bn in inflows. This performance comes despite a broader continental downturn that reflected a return to prior levels following inflated figures in 2024 caused by a single large-scale project.

African Regional Trends

FDI flows to Africa were marked by significant volatility and regional disparities. Egypt’s $11bn in inflows led the continent. Greenfield project announcements in Egypt and Côte d’Ivoire contributed to a 5% rise in the total number of projects across Africa, reaching 639.

Meanwhile, inflows to Angola reached an estimated $3bn, marking a return to positive values after nine consecutive years of net divestments. Conversely, South Africa recorded negative inflows of $6bn following a $7.2bn divestment by Anglo American PLC from Valterra Platinum Ltd.

Mozambique recorded an 80% surge in inflows to $6bn, driven by the acceleration of construction on major liquefied natural gas (LNG) projects.

Sectoral Shifts and Strategic Tech The global investment landscape in 2025 was increasingly shaped by data centres and artificial intelligence, a trend that posed challenges for lower-income countries.

Global Trends

The data centres sector accounted for one-fifth of global greenfield project values, surpassing $270bn. While the bulk of this was in developed markets, emerging economies like Egypt, South Africa, and Morocco are seeing increased concentration in technology-intensive sectors.

On the other hand, international project finance for infrastructure continued a four-year decline, falling 16% in value. The boom in renewable energy projects appeared to “run out of steam,” with global values in this sector dropping by 28%.

The 14% global increase was heavily influenced by more than $140bn in flows through major financial centres, including the United Kingdom and Luxembourg. In developed economies, FDI rose 43% to $728bn. In contrast, flows to developing economies declined by 2% to $877bn.

Three-quarters of the least developed countries (LDCs) saw stagnant or declining inflows. UNCTAD noted that lower-income countries continue to face persistent challenges related to financing constraints, elevated risk perceptions, and structural vulnerabilities.

2026 Outlook UNCTAD reports that prospects for 2026 remain highly uncertain. While easing inflation and lower borrowing costs could support a recovery in financing conditions, real project activity is expected to be weighed down by geopolitical tensions, regional conflicts, and economic fragmentation. Capital expenditure is likely to remain concentrated in a few strategic industries, particularly semiconductors and data centres.