Beltone Financial said its outlook for the banking sector remains positive despite recent regulatory reforms, thanks to strong growth opportunities.

In a research note, Beltone explained that financial inclusion is a major upside catalyst; however, clear signs of improving dynamics are not yet in sight, adding that money in circulation outside the banking sector marked its all-time low since 2003, reaching only 12.1% of M2, thanks to the government’s financial inclusion efforts; yet, it remains the highest among its regional peers.

On the individual front, it sees a major improvement in financial inclusion efforts as latest data from the World Bank (WB) showed that 32.8% of adults held bank accounts in Egypt, up from only 14% in 2014 and 10% in 2010.

“We are expecting a larger population to fall under the banking sector umbrella, reaching 65% by the end of our forecast horizon. This is supported mainly by the increasing financial literacy, stronger presence of Islamic banking, and the ongoing and projected government initiatives to boost financial inclusion for individuals,” it added.

“We are expecting a larger population to fall under the banking sector umbrella, reaching 65% by the end of our forecast horizon. This is supported mainly by the increasing financial literacy, stronger presence of Islamic banking, and the ongoing and projected government initiatives to boost financial inclusion for individuals,” it added.

However, despite such expected improvement in individuals’ financial inclusion records, Beltone is not expecting the impact on deposits’ growth to be aggressive as such anticipated growth in the number of depositors is not likely to be accompanied by large volume, since Egypt is considered to be one of the lowest per capita income in the region, with a poverty rate hovering around 32% as of December 2017.

On the other hand, studies show that Egypt’s informal economy could range between 1-1.5x.

“We believe that the major impact lies in attracting this parallel economy into the formal economy, which, in turn, will largely dampen the percentage of the money in circulation outside the banking sector. From the government’s side, as fiscal deficit is a point of attention for the time being, increasing the tax base is a major concern for the government. Hence, restructuring the tax collection process and incentivising the inclusion into the formal economy will boost the deposits’ base while increasing the money multiplier, and therefore money supply. However, we don’t expect fast improvement on this front, as the parallel economy is still plagued with several obstacles and eradicating such impediments requires a long-term plan. With this regard, the sector won’t expectedly yield full fruits during the upcoming five years,” the report read.

The investment bank, in a research note, pointed out that the new banking draft law will adversely affect the dividends of banks with small capital, and for the IFRS 9 application to have a slight impact on capital.

“Organic equity growth to support lending expansion; New Banking Law to negatively impact dividends for small banks; minor IFRS 9 impact on equity,” it said.

“Organic equity growth to support lending expansion; New Banking Law to negatively impact dividends for small banks; minor IFRS 9 impact on equity,” it said.

“We are expecting strong expansion in lending activities during the forecast horizon, particularly

led by capex recovery. Although such expansion will burden each bank’s RWA, and hence CAR,

we highly capitalise on profitability to sustain capital base levels. Moreover, the proposed new

Banking law recommends three years to increase the minimum paid in capital to EGP 5bn; we

believe EG Bank is the most negatively impacted, EXPA and Al Baraka Bank Egypt will cut their dividends

distribution, while we postpone our projected dividends distribution for Abu Dhabi Islamic Bank (ADIB) to 2023. On the other hand, we are not expecting IFRS 9’s impact on equity levels to be hefty, thanks to the last three years’ lucrative earnings growth that supported ample provision accumulation,” Beltone explained.

In the newly proposed Banking Law (currently under discussion in Egyptian Parliament), the Central Bank of Egypt (CBE) increases the minimum paid-in capital requirements to EGP 5bn for all Egyptian banks (public and private). Beltone is expecting EG Bank to be heavily affected on the back of its lower paid-in capital and retained earnings, while its profitability is not expected to safely supply the required growth in minimum paid-in capital during the upcoming three years. On the other hand, despite their lower capital base, it is expecting ADIB and Al Baraka Bank Egypt to meet the new requirements thanks to their above average market profitability and a strong parent support that highly values their investment in the Egyptian market for its higher profitability compared to other regions.

“We are expecting lower dividends’ distribution for Al Baraka Bank Egypt, Export Development Bank of Egypt (EXPA), and Housing and Development Bank (HDB) to support capital accumulation in order to meet the projected requirements. Despite its growing profitability, we are postponing our projected dividends distribution for ADIB to 2023 instead of 2021, on the back of the currently retained losses balance that is projected to be completely diminished by the first quarter (Q1) of 2020. Moreover, we are expecting a downward pressure on the banks’ ROAE on the back of higher financial leverage due to faster growth in equity levels than that of assets growth. Cost of Risk is expected to be negatively impacted on the back of higher loans growth as banks are expected to rush for lending in order to utilise their expected surge in capital base, which may negatively impact banks’ asset quality and magnify the CoR’s negative impact on profitability due to larger loans to total assets ratio. The Commercial International Bank (CIB) Egypt and QNB Alahli (QNBA) are far above minimum requirements; Faisal Islamic Bank of Egypt (FAIT) and Credit Agricole Egypt (CAE) are not expected to be negatively impacted thanks to ample retained earnings and strong earnings growth,” the report read.

“We are expecting lower dividends’ distribution for Al Baraka Bank Egypt, Export Development Bank of Egypt (EXPA), and Housing and Development Bank (HDB) to support capital accumulation in order to meet the projected requirements. Despite its growing profitability, we are postponing our projected dividends distribution for ADIB to 2023 instead of 2021, on the back of the currently retained losses balance that is projected to be completely diminished by the first quarter (Q1) of 2020. Moreover, we are expecting a downward pressure on the banks’ ROAE on the back of higher financial leverage due to faster growth in equity levels than that of assets growth. Cost of Risk is expected to be negatively impacted on the back of higher loans growth as banks are expected to rush for lending in order to utilise their expected surge in capital base, which may negatively impact banks’ asset quality and magnify the CoR’s negative impact on profitability due to larger loans to total assets ratio. The Commercial International Bank (CIB) Egypt and QNB Alahli (QNBA) are far above minimum requirements; Faisal Islamic Bank of Egypt (FAIT) and Credit Agricole Egypt (CAE) are not expected to be negatively impacted thanks to ample retained earnings and strong earnings growth,” the report read.

It added that a sustainable financial position expansion is clearly in sight, while deposits will regain their contribution to total financial position.

The Egyptian banking sector showed the fastest growth in financial position compared to the

MENA region, reaching a CAGR of 26.3% during the last five years. Such strong growth, Beltone said, came on the back of the surge in money supply as customer deposits – the main constituent of M2 – remain the sector’s core financing source. Egypt’s banks used to rely mainly on customer deposits to drive financial position growth with minimal dependency due to bank balances and other borrowing activities.

“However, prior to the EGP floatation, foreign currency (FC) shortage was a common syndrome most banks were suffering from. Accordingly, rising dependency on FC borrowing, particularly from supranational funding entities, was a common practice, resulting in higher cost of funds and lower FC liabilities’ duration given the floating nature of such borrowing activities compared to FC customer deposits. We are not expecting such exposure to remain strong in the future as deposits’ growth prospect, along with the currently prevailing FC liquidity, are expected to strengthen the deposits contribution to the total financial position. On the other hand, we believe that the growing presence of supranational funding entities is a strong asset that supports market liquidity upon which we highly capitalise our positive liquidity outlook,” the report stated.

It pointed out that money supply growth is expected to remain healthy backed by positive nominal GDP outlook.

Five years of materially changing a macroeconomic environment where inflation peaked reaching 33%, EGP floatation and aggressive increase in interest rates came in line with a surge in money supply reaching a CAGR of 21%, which has been reflected in deposits’ five years CAGR of 23.7%.

Five years of materially changing a macroeconomic environment where inflation peaked reaching 33%, EGP floatation and aggressive increase in interest rates came in line with a surge in money supply reaching a CAGR of 21%, which has been reflected in deposits’ five years CAGR of 23.7%.

Although the floatation decision amplified M2 growth rate, which resulted from translating foreign currency balances, the main driver behind the growth in M2 was the surge in local currency (LC) retail deposits’ reaching a historic contribution to M2 of 56% as of December 2018 witnessing a CAGR of 23%, thanks to public banks’ unbeatable offered rate on certificates of deposits (CDs) post floatation.

Beltone expects the average return on shareholders’ equity to shrink in 2020 by an average of 190 basis points (bps) between the banks covered by the activation of the new system to calculate the taxes on investment in debt instruments.

“Lending is to regain its pull as the primary utilisation shelters on lower interest rates and new tax amendments on government securities,” it said.

Egypt’s banking sector has one of the lowest lending utilisations in the region, thanks to the huge

sovereign exposure on the back of the expanded fiscal deficit, as banks remain the primary player in the sovereign securities market. “Our in-house macroeconomic outlook shows an increase in fiscal deficit marginally lower than our expected total assets growth, mainly on the back of the government’s fiscal reform, which will result in lower government securities constitution of total assets,” the report read.

Moreover, the newly introduced tax amendment on government securities has curbed the banks’ appetite for sovereign utilisation particularly with the current lower yield, thanks to foreign inflows. As fiscal deficit remains contained, sovereign exposure will partially decrease, providing room for lending to occupy a larger portion of total assets.

However, such a reshuffle is not expected to be dramatic as fiscal deficit is not expected to diminish in absolute terms during the forecasted period. “Accordingly, we are expecting a gradual increase in LDR, reaching 54% by 2023 resulting in loans CAGR of 14%,” Beltone noted.

However, such a reshuffle is not expected to be dramatic as fiscal deficit is not expected to diminish in absolute terms during the forecasted period. “Accordingly, we are expecting a gradual increase in LDR, reaching 54% by 2023 resulting in loans CAGR of 14%,” Beltone noted.

Beltone said that public sector and subsidised small and medium-sized enterprises (SMEs) financing is expected to keep loan growth in double digits during 2019, where the last couple of years marked a strong growth in lending activities reaching a CAGR of 18%, mainly on the back of the surge in public sector loans comprising 61% of the total growth, thanks to the energy sector and government megaprojects.

“As the government’s megaproject pipeline is still fertile and the energy sector’s expansion plans still require huge investments, we are expecting a robust growth in FC public lending to be the key driver in lending growth throughout 2019.

On the other hand, banks are obliged to meet the SMEs’ targeted weight in lending exposure

of 20% by the end of 2019. Accordingly, we are expecting SMEs’ lending to be a secondary pillar in corporate lending growth,” it added.

Covered banks deposits grew at a slightly slower 2012-18 CAGR than the total market deposits,

equivalent to 24.7% (26.7% vs total market), to reach EGP 827bn in December 2018. The bulk of this growth came mainly during the second half of 2018, capitalising on the suspension of high yield CDs offered from major public banks. Given the projected decline in interest rates, Beltone anticipates that covered banks deposits market share will be restored, especially on the retail side.

“We are expecting CIB to show the fastest growth in total deposits followed by ADIB thanks to their strong retail client base along with ambitious expansion plans. On the other hand, we believe FAIT, Al Baraka Bank Egypt, and ADIB to partially capitalise on Egypt’s lucrative potential of massive unbanked Islamic population, as their efforts to sustain and magnify their market presence are paving a way for stronger market share for Islamic banking in Egypt,” Beltone highlighted.

“We are expecting CIB to show the fastest growth in total deposits followed by ADIB thanks to their strong retail client base along with ambitious expansion plans. On the other hand, we believe FAIT, Al Baraka Bank Egypt, and ADIB to partially capitalise on Egypt’s lucrative potential of massive unbanked Islamic population, as their efforts to sustain and magnify their market presence are paving a way for stronger market share for Islamic banking in Egypt,” Beltone highlighted.

Meanwhile, banks under Beltone’s coverage constitute 22% of the market share of the total lending market, with QNBA and CIB taking the lead with 7.9% and 6.6% market shares, respectively.

“Although the prevailing market scene and the changing regulation are projected to toughen the competition over lending growth, we believe that demand on loans will accelerate given the projected growth in economic activity. We presume that covered banks will barely preserve their market shares during the forecast horizon and given the expected surge in private lending that is to be offset by the projected intensified competition over lending activities. Among our coverage, we believe the CIB, QNBA, and the CAE are best positioned to capture such an opportunity given their solid capital base and growing market presence. As for Islamic banks, ADIB enjoys the highest market share, standing at 1.4%; we expect ADIB to expand its market share given its strong corporate lending presence particularly under the bank’s new leadership and despite its relatively low capital base,” Beltone noted.

“Furthermore, we find a strong potential in retail lending activities after three years of curbed consumption levels on the back of elevated interest rates and inflation hikes. We expect retail lending to strongly pick up in 2019 on the back of lower inflation rates and anticipated increase in disposable income. On the other hand, the CBE’s growing attention to boost the mortgage lending activities will further support retail lending growth. We believe the CAE, ADIB, EGB, and the CIB will be key beneficiaries from such potential given their growing retail presence, while the HDB will largely capitalise on the CBE’s mortgage finance initiative,” it added.

“Furthermore, we find a strong potential in retail lending activities after three years of curbed consumption levels on the back of elevated interest rates and inflation hikes. We expect retail lending to strongly pick up in 2019 on the back of lower inflation rates and anticipated increase in disposable income. On the other hand, the CBE’s growing attention to boost the mortgage lending activities will further support retail lending growth. We believe the CAE, ADIB, EGB, and the CIB will be key beneficiaries from such potential given their growing retail presence, while the HDB will largely capitalise on the CBE’s mortgage finance initiative,” it added.

The investment bank also expects that the banks covered by their market share of deposits will recover in light of the expected decline in interest and the maturity of high yield certificates and Suez Canal certificates.

“With currently maturing high yield CDs and the maturity of Suez Canal certificates next September, a reshuffle in deposits market share is highly expected,” Beltone stated.

As pricing battle between banks becomes laxer on the back of the increasing attention on profitability of the main public banks, Beltone is expecting the remaining players to regain their market share after their retreat in the last three years. “Banks that successfully target customers through comprehensive and sophisticated data analytics, offer compelling products, and deliver strong digital experiences, could gain funding advantages and see contained deposit costs. On the other hand, banks with a better branch network and diversified geographical presence will benefit the most by attracting the unbanked population into the banking system,” it added.

Beltone believes that the CIB will achieve the fastest pace of growth in total deposits, followed by Abu Dhabi Islamic Bank (ADIB), thanks to their strong customer base and ambitious expansion plans.

“We flag the CAE, ADIB and QNB as our top picks on superior earnings and positive expansion outlook; but the CIB still has fruits to offer,” Beltone said.

“We flag the CAE, ADIB and QNB as our top picks on superior earnings and positive expansion outlook; but the CIB still has fruits to offer,” Beltone said.

It explained that the sector outlook remains positive despite recent regulatory updates, thanks to considerable growth potentials, favouring banks with bold ROAE, proactive ALM practices, and positive expansion outlook.

It added that ADIB trades at deep discount with P/B and P/E of 0.69x and 2.39x against ROE of 32%. It also favours QNBA’s currently positive outlook given the bank’s change in growth philosophy shifting focus to CoF optimisation.

“We assign a Hold rating to the CIB post its strong rally (27% ytd), we believe the bank’s outlook remains positive. We note that the CIB’s trading multiples’ premium level is highly justifiable given its dominant market position along with improving fundamentals. The bank trades well above its peers domestically with a P/E of 11.9x and a P/B 2.8x. We remain positive on HDB on currently higher profitability and new management team’s efforts to strengthen corporate and retail lending activities,” the report read.

“On the other hand, we see EXPA and Al Baraka Bank Egypt provide attractive valuation on unjustifiably lower multiples compared to historical levels and average peers; yet, we don’t foresee a short-term catalyst. Egypt’s banks under our coverage trade at an average of 4.3x 2018a P/E, 1.4x PB, and offer a return on equity of 29.7%, versus MENA banks (9.9x, 1.5x, 18.4%),” it added.

Credit Agricole, Abu Dhabi Islamic Bank and the CIB are expected to maintain their net interest margin in 2019, supported by the expected decrease in deposit cost.

The report noted that covered banks’ deposits grew at a slightly slower 2012-18 CAGR than the total market’s deposits, equivalent to 24.7% (vs total market 26.7%). Given the projected decline in interest rates, along with the ongoing maturity of high yield CDs and Suez Canal certificates during 2019, Beltone anticipate that covered banks’ deposits market share will be restored, especially on the retail side. “We are expecting CIB to show the fastest growth in total deposits, followed by ADIB, thanks to their strong retail client base and their ambitious expansion plans,” it explained. “On the other hand, we have seen an expansion in NIM during 2018 for covered banks thanks to higher yield on government securities. However, during Q1 of 2019, NIMs remained bold on the back of lower CoF that is mainly attributable to the continuous decrease in deposits’ duration. We are expecting the CAE, ADIB, CIB, and QNB to maintain their NIMs during 2019 backed by a projected decrease in CoF, while maintaining a positive ALM gap.”

The report noted that covered banks’ deposits grew at a slightly slower 2012-18 CAGR than the total market’s deposits, equivalent to 24.7% (vs total market 26.7%). Given the projected decline in interest rates, along with the ongoing maturity of high yield CDs and Suez Canal certificates during 2019, Beltone anticipate that covered banks’ deposits market share will be restored, especially on the retail side. “We are expecting CIB to show the fastest growth in total deposits, followed by ADIB, thanks to their strong retail client base and their ambitious expansion plans,” it explained. “On the other hand, we have seen an expansion in NIM during 2018 for covered banks thanks to higher yield on government securities. However, during Q1 of 2019, NIMs remained bold on the back of lower CoF that is mainly attributable to the continuous decrease in deposits’ duration. We are expecting the CAE, ADIB, CIB, and QNB to maintain their NIMs during 2019 backed by a projected decrease in CoF, while maintaining a positive ALM gap.”

Beltone noted that ROAA will remain bold despite the projected NIM compression to be supplemented by increasing non-interest income contribution to core banking income starting from 2021, which will further enhance the banks operating income index.

“We are expecting CIR to show a slight decline as no inflationary shocks are projected during the forecast horizon. On the other hand, as lending utilisation picks up, CoR’s negative impact on each bank’s profitability will be higher. On the ROAE level, we expect a slightly negative impact from recent tax amendments on government securities in 2019; yet, impact in 2020 ranges between c1-4ppts. Furthermore, as we are projecting RWA to occupy a larger portion of total assets, we are not expecting banks to maintain the currently elevated financial leverage ratio, which will negatively impact ROAE levels.

It believes that the return on average assets remains strong as earnings from core banking are growing, adding that the improved cost of deposits would maintain a strong net interest margin during 2019.

Sound ALM practices are expected to keep the sector’s core-banking income solid, while improving efficiency will boost the sector’s CIR on the back of easing inflation.

Sound ALM practices are expected to keep the sector’s core-banking income solid, while improving efficiency will boost the sector’s CIR on the back of easing inflation.

Moreover, Beltone highly capitalises on its positive macro outlook to contain CoR despite the growing SMEs exposure and IFRS9 implementation starting 2019.

“Accordingly, we are expecting a solid ROAA on the sector’s level weighted mainly by the anticipated improvement in profitability of public banks,” it stressed.

On the ROAE front, Beltone is expecting a slight decline in the sector’s ROAE level mainly driven by the projected lower financial leverage ratio as banks are not expected to sustain the currently high financial leverage, particularly when lending exposure regains its high contribution to financial position.

In addition, growing profitability will support capital base, paving a safe landing for the expected surge in RWA, according to Beltone.

The Egyptian banking sector enjoys continuously improving capital adequacy measures supported mainly by the organically generated capital, along with the increasing presence of supranational funding entities and strengthening parent support. Another main pillar supporting the capital base is the growing exposure toward sovereign and public business entities which exhibit lower weight in risky assets backed by the government’s support. Given our expected reshuffle in assets’ composition backed by higher private lending constitution of total assets, coupled with the expected shorter assets duration on the back of lower treasury bonds’ exposure, we foresee RWA growing faster than assets’ growth as such change in financial position dynamics will strongly weigh on credit and market risk exposures. On the other hand, we highly capitalise on banks’ growing profitability to support capital base as a consistent and sustainable source of funding.

Beltone revealed that Crédit Agricole Egypt is at the top of its list of preferred banks following its profitability and solid capital base, which supports the expansion plans of the bank and maintains the continuity of generous dividends, while it sees the CIB as making its best performance.

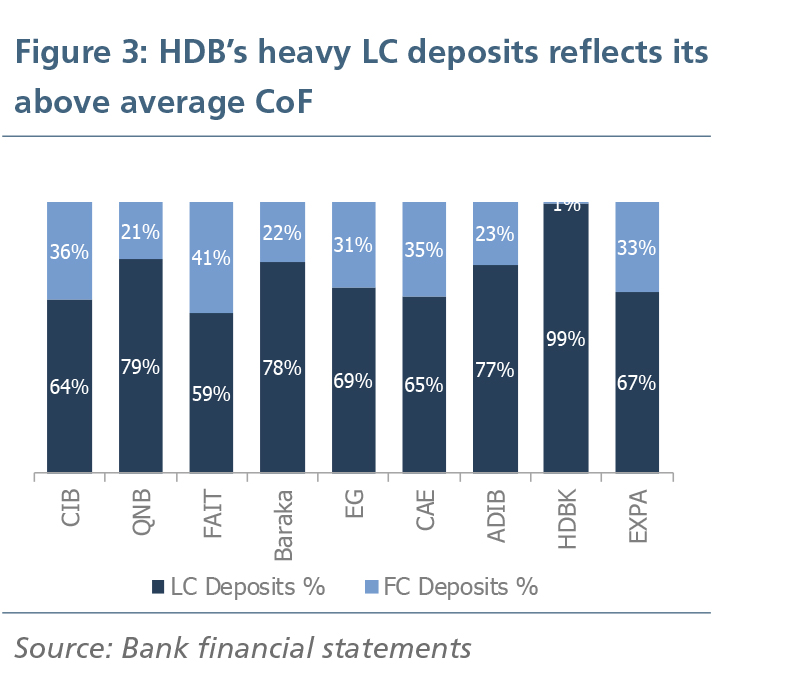

It noted that the HDB is still looking positively on its high profitability during the current period and the efforts of the management team to strengthen the lending activities of companies and individuals.

Beltone noted that six years of diminishing private lending weight on the back of heavy interest rates and the increasing weight of public debt resulted in a crowding out effect. Moreover, as cost pull inflation negatively impacted consumption levels, most companies under coverage were operating below maximum utilisation levels while pausing expansion plans on a high capex cost of debt.

Beltone noted that six years of diminishing private lending weight on the back of heavy interest rates and the increasing weight of public debt resulted in a crowding out effect. Moreover, as cost pull inflation negatively impacted consumption levels, most companies under coverage were operating below maximum utilisation levels while pausing expansion plans on a high capex cost of debt.

Beltone foresees another 100bps cut in benchmark rates during 2019. However, it is not expecting that such a decrease would trigger expansion in capex lending. Accordingly, growth in private business loans will be primarily driven by working capital financing, capitalising on improving utilisation rates while postponing capex financing to early 2020, when we are expecting another 200bps cut in benchmark.

Furthermore, the Non-Bank Financial Intermediaries (NBFIs’) expansion will toughen the competition over interest margins despite lower penetration rates where, despite the strong role the NBFIs play in the financial inclusion roadmap, their expansionary role as a financial intermediary imposes a downside risk to interest margins on loans.

Giving an insight over NBFIs, total leased contracts value grew about five folds from EGP 6.0bn in 2013 to EGP 28.6bn in 2017, according to FRA released data.

As for microfinancing, total loans portfolio reached EGP 11.55bn in 2017 versus EGP 7.1bn the prior year. These NBFIs offer a wide range of products and services to mitigate the financial intermediation gap and penetrate business areas that banks are not allowed to finance. Thereby, we do believe that these companies’ growth will continue as they diversify their products to meet more financial requirements of business enterprises, and they will carry on playing an important role for private sector loan growth.

On the other hand, banks’ appetite for utilisation in sovereign securities has been negatively affected by the introduction of new tax amendments and the decrease in government yield on the back of foreign inflows. Such change in market dynamics magnifies the aggressiveness of the competition over lending margins in terms of both interest and commissions, particularly for small cap banks, which will negatively affect the sector’s profitability. However, NBFIs provide a diversification benefit for banks which is expected to partially improve the sector’s asset quality and risk management process resulting in a contained CoR.

On the other hand, banks’ appetite for utilisation in sovereign securities has been negatively affected by the introduction of new tax amendments and the decrease in government yield on the back of foreign inflows. Such change in market dynamics magnifies the aggressiveness of the competition over lending margins in terms of both interest and commissions, particularly for small cap banks, which will negatively affect the sector’s profitability. However, NBFIs provide a diversification benefit for banks which is expected to partially improve the sector’s asset quality and risk management process resulting in a contained CoR.

Beltone projected retail lending to see strong expansion during the forecast horizon. “Retail lending activities picked up in 2018, resulting in a growth of 20%, broadly in line with total lending growth despite elevated benchmark rates. Our in-house macroeconomic outlook projects inflation to be more on the declining side following two years of a steep increase in price levels.

Moreover, after reaching a historic low level, consumption level revival is in sight given our expected growth in disposable income coupled with a contained increase in price levels. Accordingly, we are expecting a surge in retail lending backed by a revival in consumption, lower inflation, and a decrease in interest levels. Banks with strong and diversified geographical representation and ample payroll service are more likely to capitalise on such potential,” the report explained.

Supervisory measures strengthened banks’ financial soundness and role in the economy

During the last seven years, the Egyptian banking sector showed a strong improvement on almost all of its financial soundness dimensions supported by a strict supervision from the CBE allowing the sector to be a bold economic arm during economic swings. The currently improving financial soundness measures pave a way for different banking sector instruments and initiatives to safely take place in the market, including SMEs’ growing exposure, mortgage financing, e-payments, tourism sector lending, etc.

We remain positive of the sector’s soundness measures, despite the ongoing and projected instruments’ and initiatives’ expected burden, given the solid structure the system currently enjoys.